‘Death by a thousand cuts’: UK insolvencies soar 17 per cent and exceed pandemic levels

The government agency said this was higher than levels seen during the pandemic "while the government support measures were in place", with things like the furlough scheme. It is also higher than pre-pandemic figures.

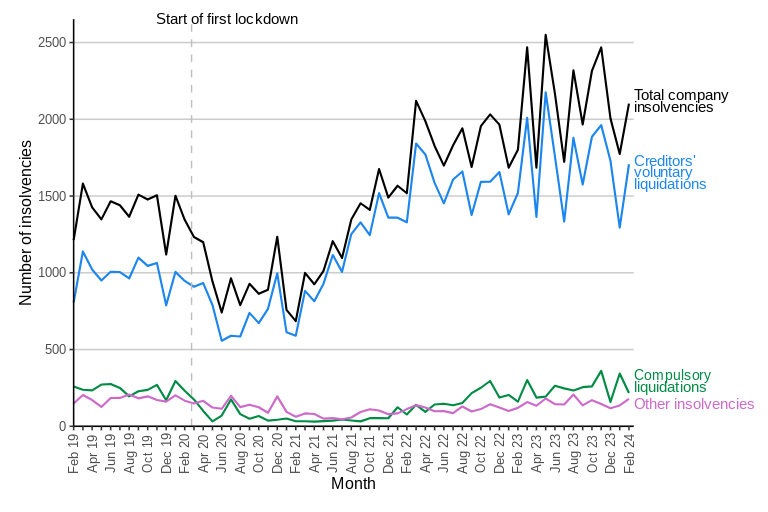

Fresh insolvency figures painted a grim picture this morning, with a number of companies going bust soaring by 17 per cent last month compared to 2023.

The government agency said this was higher than levels seen during the pandemic “while the government support measures were in place”, with things like the furlough scheme. It is also higher than pre-pandemic figures.

Analysts blamed a mixture of high inflation and the sharp increase in interest rates following the mini-budget, which increased costs of borrowing, and encouraged Brits to tighten their purses.

The war in Ukraine, which Russia launched two years ago, has also placed huge pressure on businesses’ energy costs and ability to pay rent.

It said this included 217 compulsory liquidations, 1,707 creditors’ voluntary liquidations (CVLs), 166 administrations and 12 company voluntary arrangements (CVAs).

The Insolvency Service said the numbers of compulsory liquidations, CVLs, and administrations were also higher than in February 2023.

It also said that the number of insolvencies in February 2024 was 10,136, around 23 per cent higher than last year.

This comes as the UK entered a brief recession last month, but there are already signs it had exited that period. This week it was reported the UK took its first steps out of recession after the economy returned to growth in January.

At the end of last month, S&P’s closely watched purchasing managers’ index (PMI), also showed the UK economy made a stronger start to 2024 than major European economies.

Yet, many businesses have struggled with higher interest rates, which have been on hold for some months now.

Millions of Brits are eagerly anticipating their fall, which is anticipated later this year, but some in the Bank of England’s decision-making MPC committee have been more hawkish. This week it was reported that interest rate cuts are drawing ever nearer after new data showed that slack continued to build in the labour market.

Although almost every measure suggested a softer labour market than expected, the downside surprises were small, which demonstrated the labour market was still tight in historical terms.

Julie Palmer, a partner at Begbies Traynor, said the latest data “paints an unhappy picture for the state of the UK economy”.

“This environment is putting a huge amount of pressure on businesses and the challenge business leaders now face will be insurmountable for many. “ Julie Palmer,

“After a decade of interest rates floating around zero, many businesses simply were not prepared for higher interest rates for a sustained period of time, having loaded up on cheap debt during the boom years,” Palmer said.

“Sadly, the debt storm has now broken and this morning’s data from the Insolvency Service highlights how this macro-economic environment is wreaking havoc on small and medium businesses across the country.”

She added that the latest figures would discourage business owners who had hoped interest rates might come down soon.

Daniel Staunton, a senior associate in the restructuring & insolvency team at Kingsley Napley, warned that “the facts don’t lie”.

Staunton said: “When you speak to other professionals operating in the restructuring and insolvency field they all report being busier which is reflected in the increased numbers.

“We can likely expect March 2024 stats to show another incremental increase.”

He predicted that while “new records continue to be broken” he feared it would “be an ongoing trend and whilst we won’t see tsunami levels, the total number of insolvencies this year will ebb and flow like the tide.”

Nicky Fisher, president at R3 warned that “businesses are still suffering the after-effects of last year’s economic turbulence”.

“Rising fuel, energy and funding costs and cautious consumer spending are continuing to take their toll on bottom lines and make it harder for businesses to break even,” Fisher added.

“After the pandemic era lockdowns; Brexit; staff shortages – and rising wage costs; spiralling fuel costs; high interest rates and inflation eroding consumers spending power and confidence; and the contraction in income implied by falling GDP , it is sad but unsurprising that company insolvencies have increased.” Jeremy Whiteson,

“While there is still some optimism among firms about what the next year has in store, the economic conditions remain a key area of concern for many and unless things improve, we could see more and more firms turning to an insolvency process to help resolve their financial issues. “

Meanwhile, Jeremy Whiteson, restructuring and insolvency partner at city law firm, Fladgate warned that company failures can “provoke wider economic problems if that causes unemployment or lost production”.

Whiteson said: “Against this background, the increased figures are worrying. There has been something of a ‘death by a thousand cuts’ for many businesses”, citing the impact of the war in Ukraine, the aftermath of Covid, Brexit changes and inflation.