Inflation, interest rates and tax: What happened in the economy this week?

The health of the UK economy is attracting more and more attention as the Budget draws nearer, and there was plenty for commentators to digest this week. Here’s a brief recap: What to make of this week’s news? First, the danger of inflationary persistence seems to be diminishing, with noticeable progress on both wage growth [...]

The health of the UK economy is attracting more and more attention as the Budget draws nearer, and there was plenty for commentators to digest this week.

Here’s a brief recap:

- Regular pay growth eased to 4.9 per cent, its slowest rate since June 2022. Including bonuses, pay growth was at its lowest level since November 2020.

- Reports suggested the Chancellor is planning to hike taxes and cut spending by as much as £40bn in the Budget.

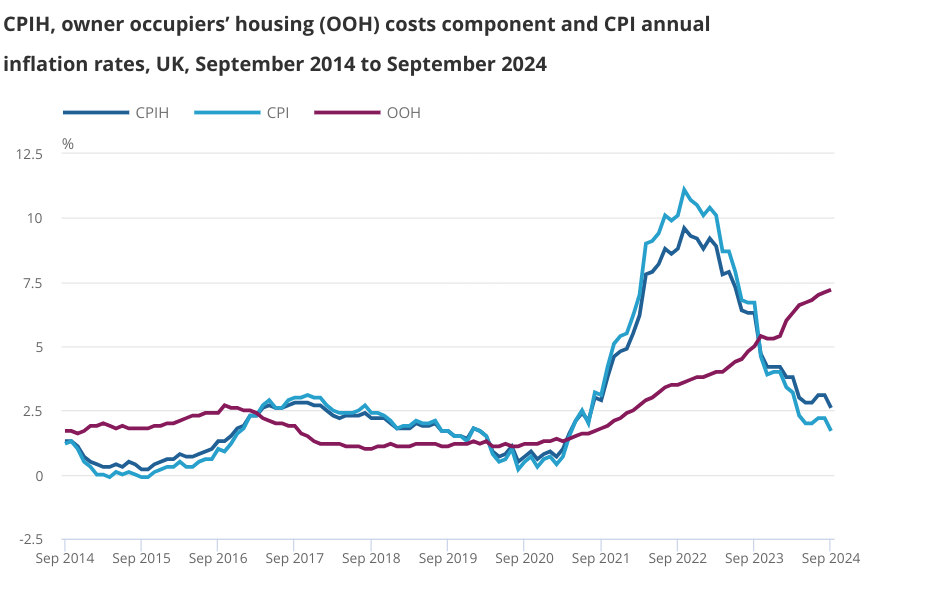

- The headline rate of inflation fell further than expected to 1.7 per cent, dragged down by easing services inflation. This brought inflation below the two per cent target for the first time since April 2021.

- Retail sales unexpectedly rose 0.3 per cent in September whereas economists had expected a 0.3 per cent fall.

What to make of this week’s news?

First, the danger of inflationary persistence seems to be diminishing, with noticeable progress on both wage growth and services inflation.

These two measures are the most important data-points for Bank officials as they try to assess the persistence of underlying price pressures in the economy.

Andrew Bailey suggested that the Bank could turn more “activist” on rate cuts if there was continued progress on inflation. He might get his way.

“The size of September’s inflation undershoot should leave Governor Bailey chomping at the bit to enact the ‘aggressive’ rate cuts he recently argued for,” Rob Wood, chief UK economist at Pantheon Macroeconomics, said.

There are caveats.

The drop in services inflation, for example, was driven by a massive 35 per cent monthly fall in airfares which will likely unwind. Indeed, economists expect inflation to climb to nearer three per cent by the year’s end.

There’s also still upside risks on wage growth, particularly if this summer’s inflation-busting pay rises have an impact on wage settlements in the private sector.

But these, at the moment, are only risks. The downward trend seems to be on track.

Following the figures traders upped bets on back-to-back rate cuts in the remainder of this year.

And with inflation falling and wage growth still relatively strong, the positive picture on the consumer side remains compelling.

This was reinforced by this morning’s retail sales figures, which showed a surprise increase in sales volumes in September. Over the past year, retail sales have increased 3.9 per cent, the largest annual increase since February 2022.

“There are now signs that there has been a gradual recovery in 2024,” Matt Swannell, chief economic adviser to the EY Item Club said, a recovery which he predicted would continue.

“Household income growth looks likely to remain solid and the labour market has been resilient, offsetting the drag from tighter fiscal policy and previous interest rate rises,” he said.

The increase in sales volumes came despite a sharp fall in consumer confidence during September, suggesting that fears about Budget tax rises have not harmed spending decisions.

Ready for the Budget?

Many commentators have chastised the new government for taking an overly gloomy view of the economy since entering office, and on this evidence they have a point.

With inflation falling, real incomes rising and more rate cuts on the way, the UK’s growth story remains intact.

That doesn’t take away from the fact that the fiscal position is deeply challenging, but it does point to relatively healthy economic fundamentals.

Which brings us to the Budget.

Having warned of a £22bn blackhole back in July, the latest reports suggest the Chancellor now wants to find an extra £40bn, mainly so that the government can increase funding for public services.

The Chancellor’s unenviable task is to try and shore up the nation’s finances without damaging the economy’s growth story.

Many business groups have warned that ramping up taxes will do exactly that.

However, most economists think it is fairly unlikely that the Budget will make much difference, at least over the short term.